{kind=link}

One bad accident can wipe out everything you’ve built as a contractor, and most of you don’t carry enough insurance to survive it. Your standard general liability and commercial auto policies max out at $1,000,000 or $2,000,000, but construction injury settlements now routinely blow past those limits. An umbrella policy sits on top of your primary coverage and kicks in when a claim exhausts your base limits, protecting your business assets and personal wealth from catastrophic losses. This guide breaks down what umbrella insurance actually covers, what it costs, and when you’re required to carry it.

What Contractor Umbrella Policies Cover and How They Work

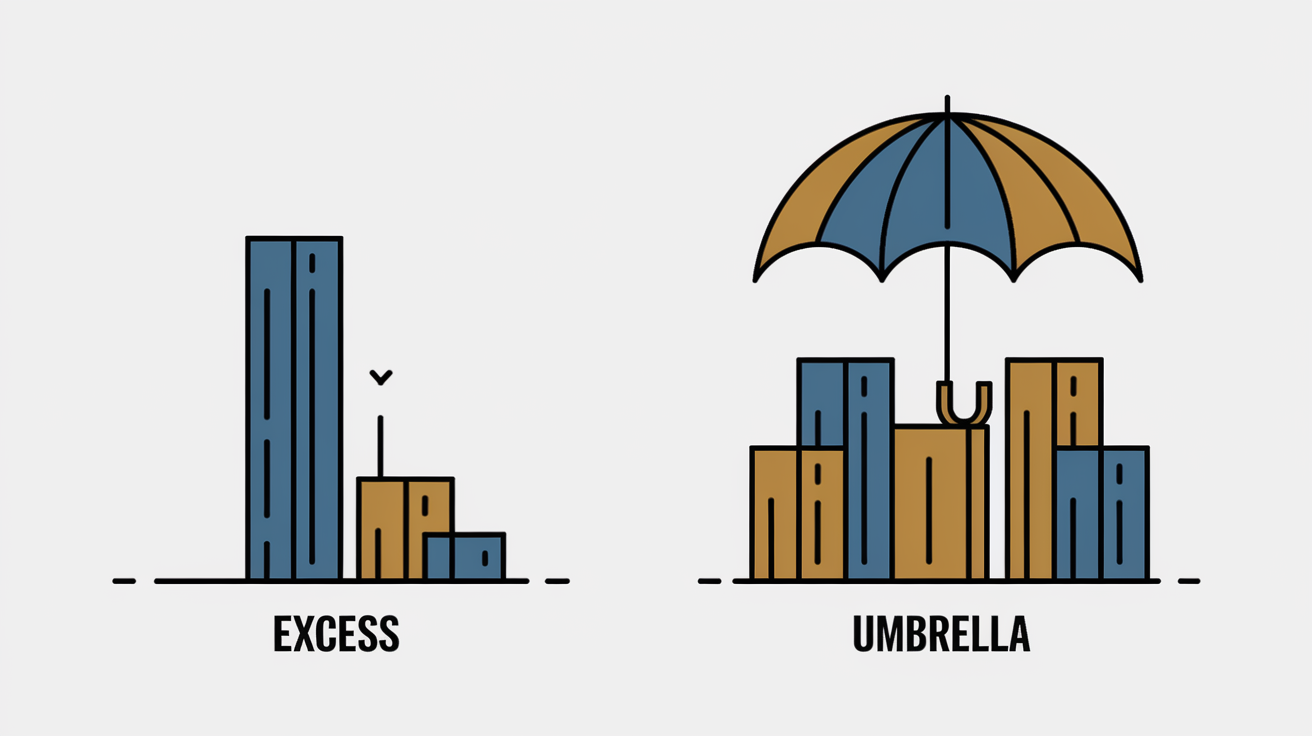

An umbrella policy is excess liability coverage that sits on top of your primary insurance policies: general liability, commercial auto, and workers compensation. It’s a second layer of protection that only kicks in after your underlying coverage runs out. When you exhaust the limits on one of those primary policies, the umbrella takes over and covers what’s left.

Here’s how the math works. If you carry a standard general liability policy with a $1,000,000 per occurrence limit and add a $1,000,000 umbrella on top, you now have $2,000,000 in total coverage per incident. The same applies across multiple policies. Let’s say you have $1,000,000 in general liability and $1,000,000 in commercial auto liability. Adding a $1,000,000 umbrella means you get $2,000,000 in coverage for either a general liability claim or a commercial auto claim, whichever one exhausts its primary limit first.

The umbrella waits in reserve until your primary policy pays out its maximum. Once that primary limit is hit, the umbrella takes over and covers the remaining damages, legal fees, and settlement costs up to its own limit. This stacking arrangement protects you from catastrophic claims that blow past what most contractors carry in standard coverage.

Umbrella policies also include drop down coverage for certain gaps in your primary insurance. If a covered claim falls into a gap that your primary policy doesn’t address, the umbrella can drop down and provide protection after you pay a self insured retention (usually $10,000 to $25,000). The policy follows form across all your underlying policies, meaning it generally mirrors the coverage terms of whichever primary policy is exhausted, then extends those protections higher.

Coverage Events and Scenarios Protected by Contractor Umbrella Insurance

Construction is one of the most hazardous industries in the country. One in five workplace deaths happens on a construction project. The combination of heavy equipment, elevation work, power tools, and coordination among multiple trades creates constant risk. When something goes wrong, the financial damage can easily exceed the $1,000,000 or $2,000,000 limits most contractors carry on their primary policies.

Real world examples show how fast costs escalate. A deck collapse at an apartment complex injured 15 people, triggering medical claims, lost wage lawsuits, and an investigation into faulty construction practices. The total cost ran past $3,000,000. A contractor’s work truck caused a multi vehicle accident on the highway, resulting in severe injuries to three people and damage to five vehicles. The settlement topped $2,500,000. Without umbrella coverage, these incidents can wipe out a business and threaten personal assets.

Umbrella policies protect against these specific scenarios:

Severe third party bodily injury claims that exceed your general liability limits, such as a subfloor failure that causes permanent disability. Major property damage disasters from construction errors, like a plumbing mistake that floods an entire commercial building. Commercial vehicle accidents involving multiple injured parties, especially when your trucks cause highway pileups or intersection collisions. Employer liability claims that go beyond workers compensation caps, including third party over actions where injured employees sue for gross negligence. Libel, slander, or advertising injury claims that arise from business disputes or public statements about competitors. Multi party lawsuits involving subcontractors, property owners, and adjacent businesses all seeking damages from the same incident.

The financial stakes keep climbing. Auto accident jury awards that used to settle around $500,000 now routinely exceed $1,000,000. Nuclear verdicts in commercial vehicle cases have reached $30 million, $50 million, and even $100 million in recent years. Medical bills and vehicle repair costs continue rising, and juries are more willing to award large sums when they see serious injuries caused by construction activity or commercial driving. Umbrella coverage is the only way to protect yourself when a claim enters that catastrophic range.

Contractor Specific Needs and Strategic Asset Protection

Umbrella insurance isn’t just about meeting insurance requirements on a contract. It’s a strategic tool for protecting everything you’ve built in your contracting business and your personal life.

Contractual and Client Requirements

Most commercial contracts and government bid specifications now require contractors to carry $2,000,000 to $5,000,000 in total liability limits. Your standard general liability policy maxes out at $1,000,000 or $2,000,000 per occurrence, which means you need an umbrella to hit those contractual thresholds. Without it, you can’t bid on the work. If you try to perform work without meeting the required limits, you’re in breach of contract and the property owner can terminate the agreement, withhold payment, or sue you for any damages that occur. The umbrella policy is what allows you to compete for larger projects and work with clients who demand higher coverage.

Rising Settlement Costs and Nuclear Verdicts

Average construction claim settlements have climbed 15 to 20% in recent years, and catastrophic incidents now routinely exceed $1,000,000 to $2,000,000 in total damages. The combination of higher medical costs, inflated property values, and more aggressive plaintiff attorneys means that what used to be a $500,000 claim now settles for $1,500,000. Juries are also awarding nuclear verdicts in cases involving serious injury or death, especially when commercial vehicles are involved. A single accident can result in a $10,000,000 or $20,000,000 judgment. Your primary policies won’t come close to covering that, and without an umbrella, you’re personally liable for the difference.

Business and Personal Asset Protection

When a judgment exceeds your insurance coverage, creditors can come after your business assets. Equipment, vehicles, accounts receivable, real estate. And in many cases, your personal assets as well. Even if you operate as an LLC or corporation, courts can pierce that protection if they find commingling of funds, inadequate capitalization, or personal guarantees on business debts. Your home, retirement accounts, and savings are all at risk. The umbrella policy shields both sides by providing enough coverage to satisfy most judgments without touching your assets. If the claim is covered, the insurance company pays, and your wealth stays intact.

Cumulative Risk Exposure Over Time

Every project you complete adds to your total risk exposure. A deck you built three years ago can fail today. A driveway you poured last year can crack and cause a trip and fall. The work you did on a commercial building can trigger a construction defect lawsuit five years from now. As you grow your business and complete more projects, the probability of a large claim increases. The more jobs in your history, the more chances something goes wrong. Umbrella coverage scales with that risk, giving you the protection you need as your portfolio of completed work expands.

Long Term Financial Security Strategy

An umbrella policy protects decades of business equity, retirement savings, and personal wealth accumulation. If you’ve spent 20 years building a contracting business, you don’t want one catastrophic claim to erase everything. The umbrella also protects your reputation by giving you the financial resources to mount a full legal defense without declaring bankruptcy. When you can afford to fight a lawsuit or settle a claim properly, you maintain your standing in the industry and keep your business operational. It’s affordable insurance compared to the alternative of losing your company and starting over.

Umbrella coverage costs a fraction of what you stand to lose in a major claim, making it one of the smartest investments a contractor can make for protecting contractor business assets.

Umbrella Insurance Compared to Excess Liability Coverage for Contractors

Excess liability and umbrella insurance sound similar, but they work differently and serve different purposes. Excess liability coverage only increases the limits on one specific underlying policy. If you buy excess liability for your general liability policy, it adds coverage only to that policy. It doesn’t touch your commercial auto or workers compensation limits.

Umbrella insurance, on the other hand, sits above multiple underlying policies and provides broader protection. A single umbrella policy increases the limits on your general liability, commercial auto, and employers liability all at once. It also includes drop down coverage for certain gaps in your primary policies, meaning it can provide protection even when your primary coverage doesn’t fully apply. The umbrella follows form, which means it generally mirrors the terms of the underlying policy that gets exhausted, but it also covers some additional claim types that might not be in your primary policies.

| Feature | Excess Liability | Umbrella Policy |

|---|---|---|

| Scope of Coverage | Limited to one specific underlying policy | Covers multiple underlying policies simultaneously |

| Number of Underlying Policies Covered | Typically one (e.g., only general liability) | Multiple (general liability, auto, workers comp, etc.) |

| Gap Coverage Inclusion | No drop down coverage for gaps in primary policy | Includes drop down coverage for certain gaps after retention |

| Additional Coverage Types | No additional coverages beyond the primary policy | May cover additional exposures not in primary policies |

| Typical Use Case | When only one policy needs higher limits | Comprehensive protection for contractors with multiple liability exposures |

For most contractors juggling general liability, commercial auto, and workers compensation, an umbrella policy is the better choice. It provides comprehensive protection across all your liability exposures without needing separate excess policies for each one.

Recommended Umbrella Coverage Limits by Contractor Size and Trade

The right amount of umbrella coverage depends on your annual revenue, the size of your projects, and the type of work you do. High risk trades and larger projects create more exposure, which means you need higher limits. Smaller contractors working low risk residential jobs can often get by with less.

Umbrella policies scale from $1,000,000 up to $10,000,000 or more, and you can adjust your limits as your business grows. The key is matching your coverage to your actual risk profile and the contractual requirements you face in your market.

Here’s a breakdown of typical coverage needs:

Small contractors under $1,000,000 in annual revenue doing residential remodels, small repairs, or finish work should start with $1,000,000 to $2,000,000 in umbrella coverage. Mid size firms with $1,000,000 to $5,000,000 in annual revenue handling commercial projects, multi family construction, or larger residential builds commonly need $2,000,000 to $5,000,000 in coverage. Large contractors over $5,000,000 in revenue working on commercial developments, industrial projects, or municipal work should carry $5,000,000 to $10,000,000 or more. High risk trades such as roofing, demolition, and HVAC installation require higher limits regardless of business size due to the severity of potential claims. Specialty contractors operating heavy equipment, cranes, or commercial truck fleets need customized high limits to match their catastrophic loss potential.

The size of your typical project also matters. If you’re working on a $10,000,000 commercial building, a $1,000,000 umbrella won’t cut it. A single construction defect claim on a project that size can easily exceed your coverage. As a rule, your total liability coverage (primary plus umbrella) should be at least 20 to 30% of your largest project value.

Consult with an insurance professional to assess your specific risk profile, review your client contracts, and determine the right umbrella limit for your business. What works for a residential remodeler won’t be enough for a commercial concrete contractor, and your coverage should reflect that difference.

Cost Factors and Premium Estimates for Contractor Umbrella Policies

Umbrella insurance premiums typically range from $500 to $2,000 per year for each $1,000,000 of coverage, depending on your underlying limits, claims history, trade, and location. That means a $2,000,000 umbrella policy might cost anywhere from $1,000 to $4,000 annually.

Several factors determine where your premium falls in that range. Number and type of underlying policies requiring umbrella coverage. If you carry general liability, commercial auto, and workers comp, you’ll pay more than a contractor with just one or two policies. Specific trade and associated risk level. Heavy construction, roofing, and demolition contractors pay higher premiums than finish carpenters or remodeling contractors. Total number of employees on payroll. More employees mean greater liability exposure and higher premiums.

Annual revenue volume. Businesses with higher revenue face larger potential claim sizes, which increases cost. Business location and regional claim trends. Contractors in litigious states or high cost areas pay more than those in lower risk regions. Personal claims history and loss runs. Clean claims history over the past five years can lower your premium, while multiple claims will drive it up. Contractors with commercial trucks in their fleet face higher costs due to significant liability exposure from vehicle accidents. Project size and complexity affecting risk assessment. Contractors bidding large commercial projects or working in hazardous environments pay more than those doing small residential jobs.

Bundling your umbrella policy with your existing general liability, commercial auto, and workers compensation coverage often reduces costs. Many carriers offer package discounts when you consolidate all your liability insurance under one roof.

The underwriting process involves reviewing your loss runs, current policy limits, payroll, revenue, and trade classification. Contractors with clean claims history and well documented safety programs can negotiate lower premiums. High risk trades like roofing, demolition, and heavy construction should expect to pay premiums on the higher end of the range regardless of business size, simply because the severity of potential claims is greater.

Qualifying Requirements and Underlying Policy Minimums for Contractors

You can’t buy an umbrella policy without first carrying adequate underlying coverage. Insurance carriers require you to maintain minimum limits on your primary policies before they’ll issue an umbrella. These minimums ensure there’s enough primary coverage in place to handle most claims before the umbrella ever activates.

| Underlying Policy Type | Typical Minimum Requirement |

|---|---|

| General Liability | $1,000,000 per occurrence / $2,000,000 aggregate |

| Commercial Auto Liability | $1,000,000 combined single limit |

| Workers Compensation Employers Liability | $1,000,000 per accident |

| Any Other Applicable Primary Policies | $1,000,000 minimum limits as required by umbrella carrier |

If your primary policies don’t meet these minimums, you’ll need to increase those limits before you can add an umbrella. Some carriers are more flexible, but most follow this standard structure. The idea is that the primary policies should be strong enough to handle the majority of claims on their own, leaving the umbrella to cover only the truly catastrophic incidents.

Your underlying policies must remain active and in good standing for your umbrella coverage to apply. If you let your general liability policy lapse or cancel your commercial auto coverage, the umbrella won’t cover claims related to those exposures. The umbrella only works when the underlying policy is in place and has exhausted its limits.

When you request a certificate of insurance for a client or project owner, both your primary limits and your umbrella limits will be listed. The certificate shows the total combined coverage you carry, which is what clients look at when they’re verifying you meet their insurance requirements. Keep your certificates updated and provide them promptly for bid submissions and contract negotiations.

Common Exclusions and Coverage Limitations in Contractor Umbrella Policies

Umbrella policies follow the form of your underlying coverage, which means they generally extend the same protections your primary policies provide. But they also have standard exclusions that apply regardless of what your primary policy covers. Some risks are simply not insurable under an umbrella, and others require separate specialized policies.

Not every claim that exhausts your primary policy will automatically trigger umbrella coverage. The umbrella carrier will review the claim to make sure it falls within the policy’s terms. If the claim involves an excluded activity or exposure, the umbrella won’t pay, even if your primary policy covered part of it.

Here are the most common exclusions in contractor umbrella policies. Intentional acts and criminal behavior, including fraud, theft, or deliberate harm to another party. Professional errors and omissions, such as design mistakes, engineering failures, or faulty plans. These require separate professional liability insurance. Pollution and environmental contamination, including gradual releases of hazardous materials or soil contamination from construction activities. Employment practices liability, such as wrongful termination, discrimination, or harassment claims by employees.

Cyber liability and data breaches, which are excluded from most umbrella policies and require standalone cyber insurance. Business owned aircraft, which are almost never covered under standard contractor umbrella policies. Claims that fall into gaps in your underlying policies but don’t meet the drop down coverage criteria in your umbrella.

Some of these exclusions can be addressed by adding endorsements to your umbrella policy or purchasing separate policies for those specific risks. For example, if you’re concerned about pollution liability from demolition work or soil disturbance, you can buy a contractor’s pollution liability policy to cover that exposure.

Review your exclusions carefully with your insurance agent and identify any gaps that could leave you exposed. If you’re doing design build work, you might need professional liability coverage in addition to your umbrella. If you’re handling hazardous materials or working on contaminated sites, pollution coverage becomes essential.

Step by Step Process for Obtaining Contractor Umbrella Insurance Quotes

Getting an umbrella quote is straightforward if you approach it systematically and work with the right agent. Most contractors can have quotes in hand within a few days by following a clear process.

Here’s how to get accurate umbrella insurance quotes. Review your existing liability policies and note the current limits on your general liability, commercial auto, and workers compensation coverage. Calculate your total liability exposure by reviewing your largest contracts, ongoing projects, and client insurance requirements. Gather your loss runs and claims history documentation for the past five years. Carriers will want to see your claims record before quoting.

Contact your current insurance agent first and request a bundled quote that includes your umbrella alongside your other liability policies. Request quotes from 2 to 3 additional brokers or independent agents to compare pricing and coverage options. Evaluate each quote by reviewing not just the premium cost, but also the coverage scope, exclusions, drop down provisions, and underlying policy requirements.

Start with your existing agent because they already know your business, your claims history, and your current coverage. They can identify gaps in your primary policies that the umbrella should address, and they can often bundle the umbrella with your other coverage for a lower premium. If your general liability, commercial auto, and workers comp are all with the same carrier, adding an umbrella is usually a simple endorsement.

Consolidating your general liability, auto, workers compensation, and umbrella under one agent streamlines policy management and improves coverage coordination. When all your liability policies are with the same carrier or managed by the same agent, claims processing is faster, coverage gaps are less likely, and you have one point of contact for all your insurance needs. This is especially important when you’re following best insurance practices for contractors and building a comprehensive risk management strategy.

Avoid split agency arrangements where one agent handles your umbrella and another manages your other liability policies. This creates coordination challenges, increases the risk of coverage gaps, delays claims processing, and leads to inconsistent policy renewals and updates. If the umbrella carrier and the primary carrier don’t communicate effectively, you can end up with mismatched coverage that leaves you exposed when a claim happens.

When Contractors May Not Need Umbrella Insurance Coverage

Umbrella insurance isn’t necessary for every contractor in every situation. If you’re running a low risk operation with small projects and minimal liability exposure, you might not need the extra coverage. At least not yet.

Solo contractors doing administrative or consulting work with no employees, no commercial vehicles, and no physical construction activity face much lower liability risk. If you’re operating as a project manager or construction consultant who doesn’t perform hands on work, your general liability policy may provide adequate coverage on its own. Similarly, independent contractors handling small residential repairs under $50,000 in project value, with no employees and basic tool use, may not face the catastrophic claim potential that makes umbrella coverage essential.

If your primary liability policies already meet all your contractual obligations and client requirements, and you’re not bidding on projects that require higher limits, you might be fine without an umbrella. Some contractors carry $2,000,000 in general liability coverage and find that it satisfies every contract they encounter. In that case, adding an umbrella would be redundant.

But understand that as your business grows, takes on larger projects, hires employees, or expands into higher risk trades, the need for umbrella coverage grows with it. What works when you’re a one person remodeling contractor doing kitchen backsplashes won’t be enough when you’re running a crew of five doing full gut renovations. Reevaluate your coverage needs annually as your business changes.

Special Considerations for Different Contractor Specialties

Different trades face unique liability exposures that affect how much umbrella coverage they need and what specific risks the policy should address. What makes sense for a plumber isn’t the same as what a demolition contractor requires.

Roofing and Exterior Contractors

Roofing contractors face constant fall risks, both for employees and for materials that can drop onto people or property below. Faulty roof installations can lead to water intrusion, mold growth, and structural damage that doesn’t become apparent until years after the project is complete. Weather related failures, like roofs that blow off in storms or leak during heavy rain, create property damage claims that can easily exceed $1,000,000. Roofing and exterior contractors should carry at least $2,000,000 to $5,000,000 in umbrella coverage, and more if they’re working on commercial buildings or large residential developments.

Electrical and HVAC Contractors

Electrical work carries the risk of fire, electrocution, and system failures that can shut down entire buildings. A wiring mistake can cause a fire that destroys a structure and injures occupants. HVAC system failures can lead to frozen pipes, mold growth from moisture problems, or carbon monoxide poisoning from faulty installations. Equipment malfunctions, like a furnace that overheats and starts a fire, create liability claims that quickly surpass primary policy limits. Electrical and HVAC contractors should carry $2,000,000 to $5,000,000 in umbrella coverage, with higher limits for commercial and industrial work.

Plumbing and Mechanical Contractors

Water damage is one of the most common and expensive claim types in construction. A single plumbing error can flood multiple floors of a building, destroy finishes, ruin contents, and create mold problems that require extensive remediation. Building system failures, like a burst pipe or a failed water heater, can cause hundreds of thousands of dollars in damage in a matter of hours. Plumbing and mechanical contractors should carry at least $2,000,000 in umbrella coverage, with higher limits if they’re installing complex systems in commercial buildings or multi family developments.

General and Remodeling Contractors

General contractors coordinate multiple subcontractors and take on broad project liability. When something goes wrong on a job, the property owner often sues the general contractor first, even if the problem was caused by a subcontractor. That makes general contractors the first target in most construction defect lawsuits. Remodeling contractors working in occupied homes face additional risks from damage to existing structures, injury to homeowners, and disputes over scope of work. General contractors and remodelers should carry $2,000,000 to $5,000,000 in umbrella coverage depending on project size and complexity.

Heavy Equipment and Demolition Contractors

Demolition and heavy equipment contractors face catastrophic risk potential from equipment failure, structural collapse, and property damage to adjacent buildings. A single mistake during a demolition can bring down the wrong structure, damage utilities, or injure bystanders. Heavy equipment accidents involving cranes, excavators, or bulldozers can cause severe injuries and millions of dollars in property damage. Contractors with commercial trucks in their fleet face extensive liability exposure from highway accidents involving their vehicles. These contractors should carry $5,000,000 to $10,000,000 or more in umbrella coverage, with limits that match the scale of their operations.

Certificate of Insurance Requirements and Client Documentation

A certificate of insurance is the document you provide to clients, property owners, and project managers to prove you carry the required insurance coverage. It lists your general liability, commercial auto, workers compensation, and umbrella limits, along with the effective dates and the name of the certificate holder.

Clients and project owners use certificates to verify that you meet the insurance requirements in the contract before they’ll let you start work. If your certificate doesn’t show the required limits, they’ll reject it and you won’t be allowed on the job site. Most commercial contracts and government bids require a certificate showing at least $2,000,000 to $5,000,000 in combined liability limits, which usually means you need an umbrella to reach that threshold.

Your umbrella coverage shows up on the certificate as a separate line item, and the certificate displays the total combined limits available under your primary policies plus the umbrella. For example, if you carry $1,000,000 in general liability and $2,000,000 in umbrella coverage, the certificate will show $3,000,000 in total general liability protection. That’s what clients look at when they’re verifying you meet their insurance requirements.

Typical client requirements call for $2,000,000 to $5,000,000 in total general liability coverage, $1,000,000 to $2,000,000 in commercial auto liability, and workers compensation at statutory limits. Without an umbrella, most contractors can’t hit those combined limits using only their primary policies. The umbrella is what closes the gap and makes you eligible to bid on the work.

Keep your certificates updated and provide them promptly for bid submissions, contract negotiations, and project kick off meetings. If your policies renew or your limits change, request new certificates immediately and send them to any clients or property owners who have your old certificates on file. Outdated certificates can cause project delays and contract disputes.

Claims Process and How Umbrella Coverage Activates for Contractors

When a claim is filed against you, the umbrella policy doesn’t activate until your primary liability coverage has been exhausted. The claims process unfolds in stages, with your primary carrier handling the claim first and the umbrella stepping in only when necessary.

Here’s how the process works. An incident occurs. Someone is injured, property is damaged, or a lawsuit is filed. And a claim is made against your contracting business. Your primary liability policy (general liability, commercial auto, or employers liability) investigates the claim, assigns legal defense, and begins settlement negotiations. The claim value is determined through investigation, medical records, repair estimates, and settlement discussions. At this point, it becomes clear whether the claim will exceed your primary policy limits.

If the claim exceeds your primary limit, the primary carrier pays out its maximum policy limit and formally notifies your umbrella carrier that the underlying policy has been exhausted. Your umbrella policy assumes responsibility for the remaining settlement amount, court judgment, and any additional legal costs associated with the claim.

During large claims, your primary carrier and umbrella carrier coordinate on legal defense strategy, settlement offers, and case management. The primary carrier continues to handle the defense until its limits are exhausted, then the umbrella carrier takes over. In some cases, the umbrella carrier will get involved early in the process if it looks like the claim might exceed primary limits, so they can participate in settlement negotiations and risk management decisions.

Having both your primary policies and your umbrella with the same insurance carrier or managed by the same agent avoids processing delays and coordination problems. When the carriers are different and the agents don’t communicate, there can be confusion about when the umbrella activates, who’s responsible for defense costs, and whether certain aspects of the claim are covered. Split agency arrangements create these kinds of issues and can slow down claims resolution when you need it most.

The umbrella serves as your last line of defense against catastrophic liability claims. Once it activates, it covers the remaining damages up to the umbrella’s limits, protecting your business and personal assets from collection actions.

State Specific Regulations and Regulatory Compliance for Contractor Umbrella Policies

Umbrella insurance requirements and pricing vary by state due to differences in licensing regulations, claim trends, and legal environments. Some states mandate minimum liability coverage for licensed contractors, and those minimums may include umbrella coverage for certain license classes or project types.

State contractor licensing boards set minimum insurance requirements as part of the licensing process. In some states, general contractors working on projects over a certain dollar threshold must carry liability coverage that exceeds what a standard general liability policy provides. For example, a state might require $2,000,000 in total liability coverage for contractors bidding on public works projects, which means you’d need an umbrella to meet that requirement and maintain your license.

Regional claim trends and lawsuit climate also affect umbrella policy availability and pricing. Contractors in litigious states like California, New York, and Florida pay higher premiums than contractors in states with lower claim frequency and smaller jury awards. Coastal states with hurricane exposure, states with high construction defect litigation, and urban areas with heavy traffic all create higher risk profiles that drive up umbrella costs.

Coverage territory limitations in your umbrella policy determine where you’re protected. Most policies cover work performed in the United States, its territories, and Canada, but if you’re doing cross border work or operating in multiple states, verify that your policy covers all your work locations. Multi state contractors need to ensure their umbrella policy follows them across state lines and complies with each state’s regulatory requirements.

Before purchasing umbrella coverage, verify your state’s specific licensing requirements, minimum liability mandates, and any special endorsements required for your trade. Consult with a local insurance professional who understands your state’s regulatory framework and can guide you through compliance. You can also review contractor licensing requirements by state to understand how insurance fits into your overall licensing obligations.

Final Words

Umbrella insurance for contractors explained comes down to this: it’s the safety net that catches claims when your primary policies max out.

The coverage stacks on top of your general liability, auto, and workers comp to create a deeper financial shield against lawsuits that could otherwise wipe out your business and personal assets.

Whether you need $1 million or $10 million depends on your revenue, trade risk, and client contracts, but most contractors working commercial jobs or managing crews should carry at least $2 million in total coverage.

Start by talking to your current insurance agent about bundling umbrella with your existing policies. That keeps everything coordinated and prevents gaps that split coverage creates.

FAQ

What is contractor umbrella insurance and how does it work?

Contractor umbrella insurance is excess liability coverage that sits above your primary insurance policies like general liability, commercial auto, and workers compensation. It activates when your underlying policy limits are exhausted by a claim. If you carry $1 million in general liability and add a $1 million umbrella, you get $2 million total coverage per occurrence.

When does umbrella coverage actually kick in for contractors?

Umbrella coverage kicks in after your primary insurance policy pays its maximum limit on a covered claim. If a lawsuit judgment hits $1.5 million and your general liability maxes out at $1 million, the umbrella pays the remaining $500,000 plus ongoing legal defense costs.

What’s the difference between umbrella and excess liability insurance?

Umbrella insurance provides broader protection across multiple underlying policies and includes drop-down coverage for gaps, while excess liability only increases limits on one specific policy. Umbrella follows form across general liability, auto, and employers liability, making it more versatile for contractors managing multiple liability exposures.

How much umbrella coverage do small contractors need?

Small contractors with under $1 million annual revenue typically need $1 million to $2 million in umbrella coverage. Mid-size firms doing $1 million to $5 million in revenue should carry $2 million to $5 million, while high-risk trades like roofing or demolition need higher limits regardless of company size.

What does contractor umbrella insurance actually cost per year?

Contractor umbrella insurance typically costs $500 to $2,000 per year for each $1 million in coverage. Your premium depends on your trade type, claims history, number of employees, annual revenue, and how many underlying policies you’re covering. Roofing and heavy construction contractors pay more than finish carpenters.

Do I need underlying insurance before buying an umbrella policy?

You need underlying insurance with minimum limits before buying an umbrella policy. Most carriers require at least $1 million per occurrence and $2 million aggregate on general liability, plus adequate commercial auto and workers compensation coverage. The umbrella only works if these primary policies stay active.

What claims are not covered by contractor umbrella policies?

Contractor umbrella policies don’t cover intentional acts, professional errors and omissions, pollution and environmental damage, employment practices claims, cyber liability, or business-owned aircraft. Some gaps in underlying coverage may not trigger drop-down provisions, so review exclusions carefully with your agent before purchasing.

Can sole proprietor contractors skip umbrella insurance?

Sole proprietors doing low-risk work like small residential repairs under $50,000 with no employees or equipment may not need umbrella insurance. But if you’re bidding commercial jobs, working high-value residential projects, hiring subcontractors, or operating heavy equipment, umbrella coverage becomes essential for asset protection.

How do I get umbrella insurance quotes as a contractor?

Start by contacting your current insurance agent who handles your general liability and auto policies. Gather your loss runs, claims history, and current policy declarations, then calculate your total liability exposure from active projects. Request quotes from two to three brokers, comparing coverage scope and exclusions alongside premium costs.

Why do roofing contractors need higher umbrella limits?

Roofing contractors face catastrophic fall risks, extensive property damage potential from leaks, and weather-related liability that routinely generates claims exceeding $1 million to $2 million. Most roofing operations should carry $5 million to $10 million in umbrella coverage regardless of business size or annual revenue.

What happens if my primary insurance and umbrella are with different agents?

Split agency arrangements where one agent handles umbrella and another manages your other liability policies create coverage gaps, coordination challenges, and delayed claims processing. Consolidating general liability, auto, workers compensation, and umbrella under one agent streamlines management and prevents disputes during large claims.

Do commercial contracts require contractors to carry umbrella insurance?

Many commercial contracts and government bids now require contractors to carry $2 million to $5 million in total liability limits, which means you need umbrella coverage on top of standard $1 million general liability policies. Your certificate of insurance must show combined limits meeting bid specifications.

How does the claims process work when umbrella coverage activates?

When a claim exceeds your primary policy limits, your general liability carrier investigates first, provides initial defense, and pays its maximum limit. Then the carrier notifies your umbrella insurer, who assumes responsibility for the remaining settlement amount, court judgment, and ongoing legal defense costs through resolution.

Does umbrella insurance protect my personal assets as a contractor?

Umbrella insurance protects both business equity and personal assets like your home, vehicles, and retirement accounts from lawsuit judgments. Even with an LLC, some judgments can pierce business protections, making umbrella coverage your last line of defense against catastrophic claims threatening everything you’ve built.

What underlying limits do I need before adding umbrella coverage?

You typically need $1 million per occurrence and $2 million aggregate on general liability, plus adequate commercial auto liability and workers compensation employers liability coverage. Your umbrella carrier will specify exact minimum requirements, and all underlying policies must remain continuously active for umbrella coverage to apply.